A deep understanding of Chinese TFP

Authors: JARI MATTHEW ROMAN and ÓSCAR MÁRQUEZ

Download the full article below:

ABSTRACT

China has surprised the world with unprecedented economic development in such a short period of time. Averaging annual growth of 5 percent, transforming from a rural agricultural society to an urban industrial one, from a planned to a market-based economy, and lifting out of poverty millions of people (Zhao, L. B. (2020)). This has been possible due to economic and social reforms that led to an increase in TFP (Sun, Z. a. (2011)). This paper aims to explain the dynamics of long run economic growth and acknowledge the importance of the TFP. Then this theory will be applied to the Chinese decreasing tendency on productivity by discussing the main factors of its slowdown.

1. INTRODUCTION

1.1 Objective

This paper aims to provide an overview on the Chinese TFP evolution for the last four decades by explaining the roots of it and the contributions to output per worker. This overview will aim to understand why Chinese TFP decreases today.

1.2 Structure

Our study on this topic has been divided into three main sections. First a brief contextualization of China, followed by a theoretical review on the Solow-Swan Growth Model where a great emphasis on technological progress has been discussed. Finally, a discussion on Chinese TFP will be developed by showing its roots and main factors of the slowdown.

2. A BRIEF OUTLOOK OF CHINA

The fall of the USSR has settled the economic homogeneity of the United States globally but today the Chinese are rising and breaking the solo ride of the Americans. China’s empowerment started early this century when Beijing joined the WTO in 2001 meaning that China had the privilege of having the security of trading rules but also the commitment to open their market. Exports as a share of GDP increased from 20% to a maximum of 36% in 2006. Furthermore, Chinese GDP relative to US GDP has increased from 12% to 70% in two decades thanks to high GDP growth rates during the past two decades averaging 5.24%1.

Nonetheless, China is far away from US standards. When it comes to GDP per capita, Americans are six times richer than Chinese. Moreover, China is not considered a high-income country yet despite its unprecedented growth. In terms of economic development, China ranks 85th in the HDI index and 100th in the Social Progress Index, underperforming on environmental quality, personal rights, and inclusiveness.

3. THE SOLOW-SWAN MODEL AND TFP

3.1 Defining the Solow-Swan Model

The Nobel Prize winner Robert Solow developed the first neoclassical growth model which is the basis for the modern theory of economic growth today. The Solow Growth Model is an exogenous model of long-run economic growth that involves the evolution of the level of output in an economy over time given the dynamics of the most important factor: capital, but also considering the dynamics of population growth rate, savings rate, and the rate of technological progress. The most basic assumptions of this model are the following:

- The economy is closed and it only produces one good; there is no role for the government which implies savings to be equal to the investment, there is full employment.

- There are constant returns to scale, which makes the production function homogeneous of the first degree. This means that increasing factors of production will make the same amount of increase in output.

- The two factors of production, labor, and capital, are priced according to their marginal productivity and they are substitutable for each other.

- Prices and wages are fully flexible.

- The change in the capital will basically depend on investment and the depreciation of capital.

- The labor force grows at a constant exogenous rate of “n”.

- The saving rate (s) is constant, between 0 and 1, which will be a proportion of the production function which turns out to be the income. Therefore, “s” will explain the average propensity to save.

3.2 Dynamics of the Solow Model

The output (Y) of an economy depends on capital (K), labor (L), and technology (A). However, the only state variable (variable containing all information describing a system (the economy) and its future evolution) which is also the only endogenous variable is capital (K). Hence, considering the law of motion of capital, the economy will grow as long as the change in the capital stock is positive (investment minus depreciation). In other words and fundamentally speaking, as long as agents save, investment for capital will enable economic growth. The accumulation of capital will guarantee growth until savings equal depreciation of capital (𝛾K), in this situation the economy will be on the steady-state (K, Y) therefore output growth will be null as well. When the scenario is in per capita terms, growth will be guaranteed until savings equal depreciation plus population growth. And when the scenario is in per capita efficiency terms, growth will be guaranteed until savings equal depreciation plus population growth and technological progress growth.

3.3 Defining the dynamics of the total factor of productivity

It seems that capital is the only factor that leads economic growth, however, the factor that may guarantee economic growth regardless of other inputs is technological progress (A) also known as the total factor of productivity. The roots of the total factor of productivity (TFP) are related to the Solow Residual concept. Output growth is a mix of the growth of the following factors: labor, capital, and technical progress. The latter turns out to be the growth of the efficiency in the utilization of the aforementioned factors which is also known as Solow Residual (for now on TFP). TFP is a complex variable to estimate since it cannot be observed, therefore its estimation comes from observable variables such as labor, capital, and output and that is why it is also called Solow Residual because it can only be known after estimating the observable variables.

Assuming a Cobb-Douglas production function, the output would be a function of capital, labor and TFP hence the latter’s growth rate (a) would conversely depend on the growth rate of output (𝑔𝑦), capital (𝑔𝑘), and educational attainment and the return to each additional year of education (𝑔ℎ) which symbolizes labor. Moreover, considering α as the intensity of capital in the economy, the growth rate of the economy and the TFP could be computed as follows:

Notice that the role of population growth does not contribute directly to output since what really matters is the educational attainment and the return to each additional year of education of the population for long-term economic growth.

Considering that TFP goes up, it will imply an increase in the production function and consequently to savings (sy). Therefore, the economy would not be in the steady-state anymore since the Law of motion would be positive provoking an expansion of capital (k) towards a higher steady-state of capital (k). As capital is converging to k, at a slower pace due to diminishing marginal returns, output (y) will do so to its new steady-state of output (y*). Overall the economy is much more efficient in using fewer inputs to obtain the same output. This is the main reason of technological progress importance since it is the only factor that may sustain long-run economic growth. However, an increase in the depreciation rate (𝛾) and/or population growth (n) may offset the effect of TFP in the economy since capital would depreciate faster and the ratio of capital and labor will decrease causing a decrease in labor productivity. Furthermore, in real life, aggregate TFP growth can be improved by two mechanisms (Restuccia and Rogerson (2013)):

- Reallocating resources between firms, by either:

2.1 Moving resources between existing firms.

2.2 The entry and exit of firms. - Raising productive efficiency within firms by either:

1.1 Innovating.

1.2 Adopting more efficient existing technologies.

By considering these mechanisms an economy may pursue long term economic growth enabling citizens to be wealthier.

4. ANALYZING CHINESE TFP

4.1 An outlook of Chinese TFP

In 2016 Chinese GDP growth started to fall after more than two decades of growth rates above 7%2. This was in fact due to a slowdown of aggregate TFP that was 2.80% the decade before the Great Recession and fell to 0.70% the decade after (Zhao, L. B. (2020)). However, in order to understand this phenomenon, it is good to know how the Chinese TFP could have been so large compared to what it is today.

At the end of the 70s, the Chinese government implemented economic reforms which symbolized the Basis for modernization and better effectiveness of institutions resulting in what is China today. Moreover, it can be distinguished from four areas of intervention in these reforms: 1. Market reforms by enhancing property rights, 2. Provide more space to the development of private firms to step forward to technology production, 3. Investment in human capital by increasing the quality of education and 4. Reinforce market signaling to attract foreign investment such as positive trade balance or increasing domestic demand. For instance, SOEs (State-Owned Enterprises) were given more autonomy and non-SOEs were allowed to enter the market, creating competition. Moreover, in the 90s, China prioritized ownership reforms, including passing the 1992 Company Law and 1993 Competition Law and developing an institutional Framework for a business sector with diversified ownership. In addition, foreign companies started to transfer technology with license agreements and selling equipment nourishing the Chinese economy with capital. Furthermore, and administratively speaking, special economic and technological areas were set up till developing to what is known as Shenzhen or Hong Kong for instance.

The 21st century China developed mid and long-term plans for science and technological development which aimed to depend less on importing technology and transition to a high valuedadded export country, particularly in the technological sector. For that reason, gross domestic spending on R&D increased 12-fold in less than 20 years3 while patent registration tripled in almost a decade4. All in all, innovation was starting to be led by the private sector while the Government just aimed for flagship projects such as the Road and Belt initiative that will enable them to provide these high-tech Chinese products to the world.

As a result of these structural reforms, between the 80s and the Financial Crisis, output per worker growth came from a more relaxed capital deepening, meaning that labor is much more productive. But after 2008, growth has been significantly based on capital accumulation which accounted for over 80% of output per worker growth (Figure 4). Indeed, this was due to higher investments particularly from the Government through fiscal stimulus packages to cope with the Great Recession and the 2015-16 growth slowdown. So even the share of TFP to output per worker growth has drastically fallen, it was induced not only by a decrease in aggregate TFP but also by an increase in physical capital through investment. When it comes to human capital, this factor does not play a significant role in output per worker growth.

4.2 Factors on the slowdown in TFP growth

4.2.1. Labor force (re)allocation

Knowing that the behavior of TFP affects the outcome of the growth of output per worker we will focus on in the latter since as mentioned before TFP itself is complex to estimate. What is interesting on the growth of output per worker, also known as labor productivity is that it can be broken down into sectoral movements. Timmer et al. (2015) manage to decompose changes in productivity within sectors and across sectors. For China, labor productivity within sectors contributed 78% to the aggregate labor productivity growth rate and the rest were labor productivity across sectors (1979-2018) (Figure 5.). Therefore, this result shows that output per worker growth can be mainly explained by a better reallocation of workers in the same sector meaning that overall TFP contributed to labor productivity by raising productive efficiency though more specifically adopting more efficient existing technologies.

The reallocation was possible thanks to the aforementioned market reforms that allowed the economy to run more efficiently. In the labor market that means the labor force has shifted to more efficient companies, which had better property rights and high investment for capital deepening, mainly within sectors, enabling the development and maturing of the secondary and tertiary sectors. All in all, from a Solow-Swan model perspective, the Chinese production function shifted up over time due to higher efficiency as a response to the reforms.

Nonetheless, the output per worker growth rate slowdown experienced after the Great Recession at a global level, particularly in advanced countries due to a declining effect of the information and communication technology boom, an aging workforce, slower human capital accumulation, and slowing global trade integration (Adler et al., 2017) also affected China’s output per worker growth rate negatively. The reason for it, aside from these exogenous factors, is the fact that labor is moving towards low productivity service sectors such as trade, restaurant and hotel, and nonmarket services. This may be explained by the theory of diminishing marginal returns. Indeed, the reallocation of the labor force towards productive sectors that started decades ago may be starting to be saturated such that an additional worker in the service sector is being less productive than its predecessor.

This logic may have its flaws but it is important to mention that within the service sector, employment in high productivity service sectors such as finance, real estate, and business services accounts for only 1% of total employment during the last four decades meaning that the services sector is increasing in the labor force but is marginally less productive. Furthermore, after the Great Recession, investments were constrained and credit conditions were tighter5 which in the SolowSwan model perspective if these constraints are maintained lower investment would mean lower capital accumulation hence lower output. Moreover, if the labor force in the service sector is constantly increasing, capital per worker will in fact decrease and consequently labor productivity. Not to mention that technological progress is highly correlated to capital accumulation. Constraints on the financial sector, as happened after the Great Recession, may slow the pace of capital investment.

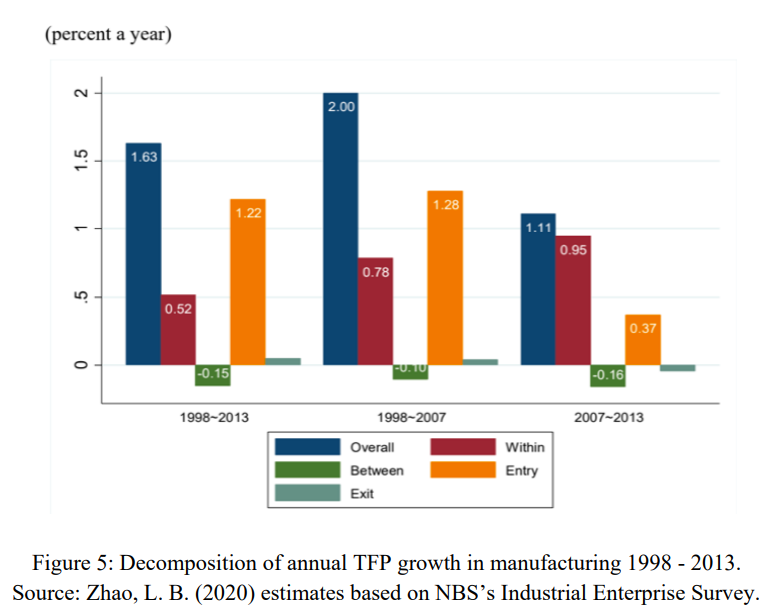

4.2.2. Firms in the manufacturing sector

Chinese average TFP growth in the manufacturing sector before the Great Recession came from a net new entry of firms that accounted for two-thirds of aggregate TFP growth (Figure 6) while the rest was a factor of raising productive efficiency within firms (Brandt et al., 2012) meaning that the productivity from the manufacturing sector came from the reallocation of resources between sectors and firms. This new massive entry, specifically in the 90s and 00s was due to the aforementioned goal of China to lead the country to a highly valued-added export economy which enabled the private sector to flourish.

With the available data between late 90s and the Great Recession, the reasoning behind the increase in TFP growth is due to the fact that new firms contribute to TFP positively if their productivity is higher than the average productivity of the existing firms. Analogously, the exit of low productive firms should raise productivity.

Moving on to more recent times, average manufacturing productivity growth in China decreased almost by half after the Great Recession. This was caused by a dramatic decline in new entry productive firms because of 1. New entrants had lower productivity than the average, 2. There were fewer new firms, 3. Financial factors such as credit access were tight. Consequently, average manufacturing TFP growth reversed and relied on the rise of productive efficiency of existing firms.

In contrast, the reallocation of resources in the manufacturing sector had no gains, in fact, it was slightly negative in the sample period. However, if the entry of new and more productive firms runs out, Chinese productivity growth can rely on improving resource allocation between firms in the future as most advanced economics do.

4.2.3. Lower efficiency on aggregate investment and credit

Technological progress is correlated with capital formation since, in order to be more efficient, investment in capital has to be made. However, in China’s case it should be considered that its economy is not considered developed yet but has a considerable capacity for R&D and capital investments. One way to measure the production efficiency of a country is by measuring the incremental capital-output ratio (ICOR) that explains the marginal unit of capital or investment needed to produce an additional unit of output. Therefore, a low ICOR is preferred as it indicates a country’s production is more efficient.

As for China, the evolution of ICOR has been positive, meaning that the investments have brought lower returns to growth. Knowing that TFP has been deteriorating alongside, China’s economy is facing today a trajectory of lower production efficiency in pretty much all senses. Chinese’s ICOR increase came mainly from the lower returns to capital in the infrastructure and real estate sectors where their sectoral-level ICOR doubled and increased by 56% respectively.

Moreover, these two sectors have also experienced higher leverage that were contributed by public investment stimulus. In fact, credit to the non-financial sector grew by more than twice the pace of GDP. This recent and rapid expansion in credit to the non-financial sector may have hindered productivity growth due to: 1. Bad allocation: the credit that went to infrastructure and housing has reduced the resources available to higher-productivity sectors and firms (Huang et al., 2017); 2. Indebted sector: a rowing non-financial sector debt, at 250 percent of GDP in 2019, may slow down growth, if deleveraging does not take place (Reinhart et al., 2012). Not to mention the market signaling this debt is exposing in the financial market, where risk premia may increase and drive interest rates up and consequently discourage investments.

5. CONCLUSION

It is undeniable that China is catching-up with high-income countries and it can be verified by the Solow Swan Model since it is converging towards levels such as the USA. Since the 70s China implemented unprecedented structural reforms that put the seeds to become the economy that it is today. Private initiatives, export of high technological valued-added products, expenditure on human capital or investments in R&D are some of the key factors that made possible TFP increase in China, thus enabling the economy to be sustained in the long-run. Or from a theoretical perspective, the Chinese production function shifted up over time thanks to its higher efficiency as a response to the reforms.

The high levels of Chinese TFP growth before the Great Recession at 2.80% were basically thanks to rising productive efficiency by adopting more efficient existing technologies and by the entry and exit of firms. From the labor market side, the labor force was allocated to firms that simultaneously adopted efficient technology thus enabling human capital to be more productive up to this day. From the manufacturing sector side, the flow of entry and exit of firms made Chinese manufacturing more productive since firms with higher capacity to compete stayed in the market and let the average productivity increase. As a result of that, production recalibrated overtime towards high value-added goods.

In contrast the inevitable Great Recession and the 2015-16 global slowdown put pressure on Chinese TFP. The tightening on the access of credit put a constraint on the entry of new firms regardless of their productive capacity. In addition, existing firms were indebted, especially sectors relativity low productive such as real estate and construction causing a bad allocation of capital. When it comes to the Chinese labor force, the matured service and manufacturing sector has been developed thanks to the already mentioned adoption of efficient existing technologies. However, when new adoptions run out and the massive shift of labor to these sectors of the economy makes every unit of labor less productive it is normal to see an overall slowdown in productivity.

In order to achieve the levels of TFP growth previous to the Great Recession, the labor force in the service sector should be reallocated to more productive sectors such as finance and business services since it only accounts for 1% of total employment. Meanwhile, when it comes to the manufacturing sector, TFP may increase by reallocating resources between the existing firms for instance by merges as happened in the Spanish banking sector after the Great Recession. In addition, the Chinese may prepare their economy by raising productive efficiency within firms by innovating domestically since trying to increase TFP through pure innovation is costly and not immediate.

- World Bank data ↩︎

- World Bank Database ↩︎

- OECD data ↩︎

- World Intellectual Property Organization data ↩︎

- World investment growth rate on non-financial assets has not recovered from the rates before the Great Recession (World Bank Data). ↩︎

6. BIBLIOGRAPHY AND OTHER SOURCES

- Solow, R. M. (1956). A Contribution to the Theory of Economic Growth. The MIT Press.

- Sun, Z. a. (2011). The role of total factor productivity in China’s economic growth.

- European Journal of International Management.

- Swan, T. W. (1956). Economic Growth and Capital Accumulation. The Economic Society of Australia.

- Zhang, Y. (2017). Productivity in China: Past Success and Future Challenges. AsiaPacific Development Journal.

- Zhao, L. B. (2020). China’s Productivity Slowdown and Future Growth Potential. WORLD BANK GROUP.

- System and Software Engineering. (February 18, 2008). CHINA, el nuevo campeón mundial del I+D+i. “De porque a GTD le interesa este gran país” https://www.gtd.es/es/blog/china-el-nuevo-campeon-mundial-del-idi-de-porque-gtd-leinteresa-este-gran-pais (Consulted on November 27, 2021).

- Bolsa de Comercio de Rosario. (May 19, 2021). La ruta china hacia su independencia tecnológica. https://www.bcr.com.ar/es/sobre-bcr/revista-institucional/noticias-revistainstitucional/la-ruta-china-hacia-su-independencia (Consulted on November 23, 2021).

- Cuenca A. (February 28, 2021). Tecnonacionalismo, la estrategia de China para ser una potencia tecnológica. https://elordenmundial.com/tecnonacionalismo-estrategia-chinapotencia-tecnologica-gepolitica/ (Consulted on November 23, 2021).

A. APPENDIX

The contents are masterpiece. you’ve done a excellent task on this subject!

Thank you so much!

It is very comforting to see that others are suffering from the same problem as you, wow!

Thanks for thr great article!

Thank you so much!